“It is my great hope someday, to see decision makers rediscover what the ancients have always known.

Namely that our highest currency is respect.”

Namely that our highest currency is respect.”

Stay in the LoopWelcome to TradingCBDC.com

A place to learn about CBDC: Central Bank Digital Currency Note: this is the 1st draft of the site and we will be adding more content and going live as time goes by. Table of contents:

1. Why are CBDCs created?

2. Types of CBDC 2.1 What is Wholesale or Commercial CBDC (W-CBDC)? 2.2 What are retail CBDC? 2.3 What are Hybrid CBDC? 2.4. What are intermediary CBDCs? 2.5. What are synthetic or indirect CBDC (sCBDC)? 3. How do central banks view CBDC? 4. What CBDCs do central banks study and test? 5. CBDC Tracker 6. World CBDC Race 6.1 China leads the CBDC race 7. Big Analytical Reports on CBDC 8. Sources Why are CBDCs created?CBDC (Central Bank Digital Currency) — digital currency of the central bank.

This is an electronic obligation of the monetary regulator, denominated in the national unit of account and serving as a means of payment, measure and conservation of value. Experts are already citing central bank digital currencies (CBDCs) as one of the most important trends that will shape the future of money in the next decade. According to a report by the Bank for International Settlements, as of early 2019, 70% of central banks were engaged in CBDC research. Due to the coronavirus pandemic, the work on creating digital currencies in different countries will only accelerate. Why do governments around the world rely on CBDC? How digital currencies differ from traditional fiat? What conclusions have central banks drawn from research and experimentation? - -Few central banks plan to issue digital currency within five years, but several institutions have already conducted or are in the process of conducting in-depth pilot trials. - -The first experiments with CBDC showed that the process requires the participation of the private sector in order to be competitive and adaptable to technological change. - -Most proposals for issuing CBDC involve the creation of a two-tier monetary system: the central bank issues and controls the turnover, and licensed intermediaries (banks and other financial institutions) distribute and provide operations. - -The claim that CBDC will rule out anonymity is unwarranted. The ECB recently investigated the possibility of anonymizing transactions using "anonymity vouchers" on the blockchain. With transfers in the blockchain, such transactions were able to be made private. - -Private stablecoins and CBDC are not mutually exclusive, but complementary. Incentives for the release of CBDC

Today, central banks already practice virtual currency emission, and a significant proportion of payments and transfers are made in non-cash form. The differences between CBDC and the existing system are as follows: - CBDC will simultaneously increase competition and stability of the financial sector against the background of banks squeezing technology companies and cryptocurrencies. - CBDCs can improve financial inclusion as they can offer new payment infrastructure with lower transfer costs. It will also make it easier for central banks to operate in a digitized economy. - Digital currencies will expand the fiscal policy instruments available to regulators for example, they will help avoid the "zero rate trap". Due to the programmability and transparency of CBDC, it is easier for regulators to control the work of deposits and loans at negative rates. More transparent data on payment flows will improve the quality of macroeconomic statistics. - CBDCs also stimulate the use of local currency to pay for goods and services, which is especially important in countries prone to "dollarization". - The "commercial" version of CBDC (when digital currency is available only to banks) will reduce settlement risks, ensure round-the-clock availability of liquidity for banks, reduce costs for cross-border transfers, etc. The motivation for CBDC research and development varies by jurisdiction. In advanced economies, central banks see digital currency as a means of increasing security and resiliency, as well as the efficiency of domestic payments and achieving financial stability. For central banks in emerging economies, achieving financial inclusion is important. |

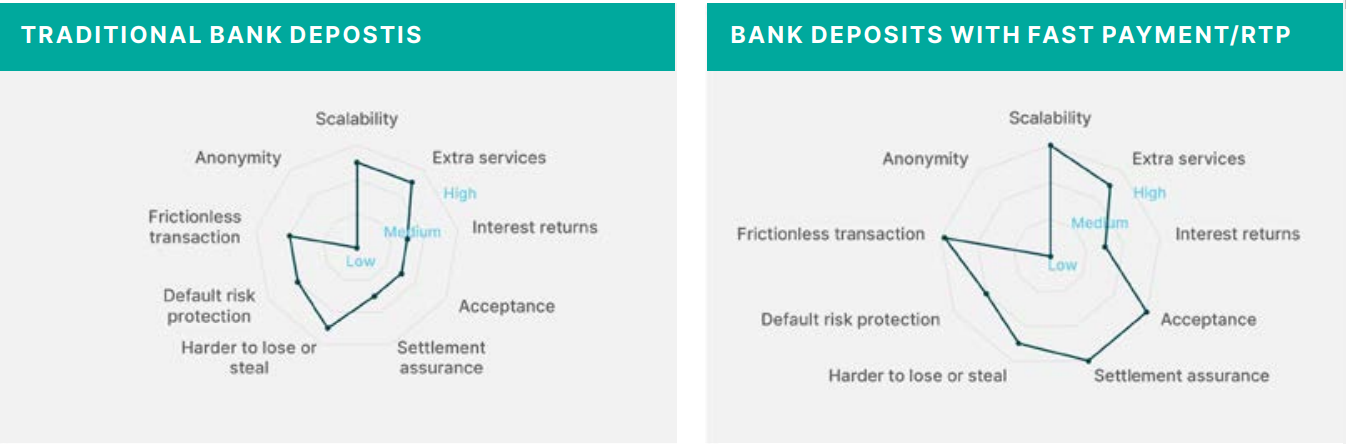

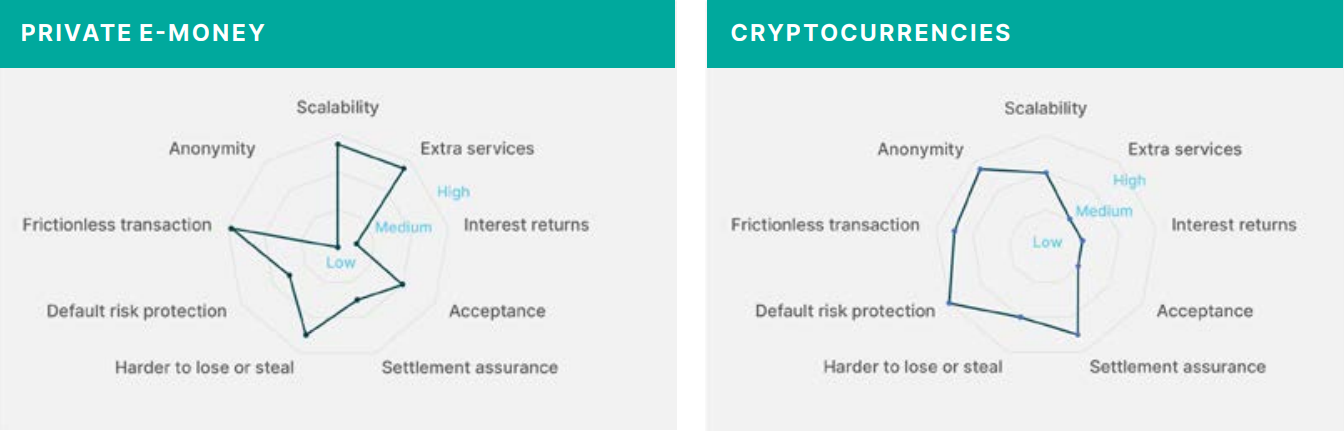

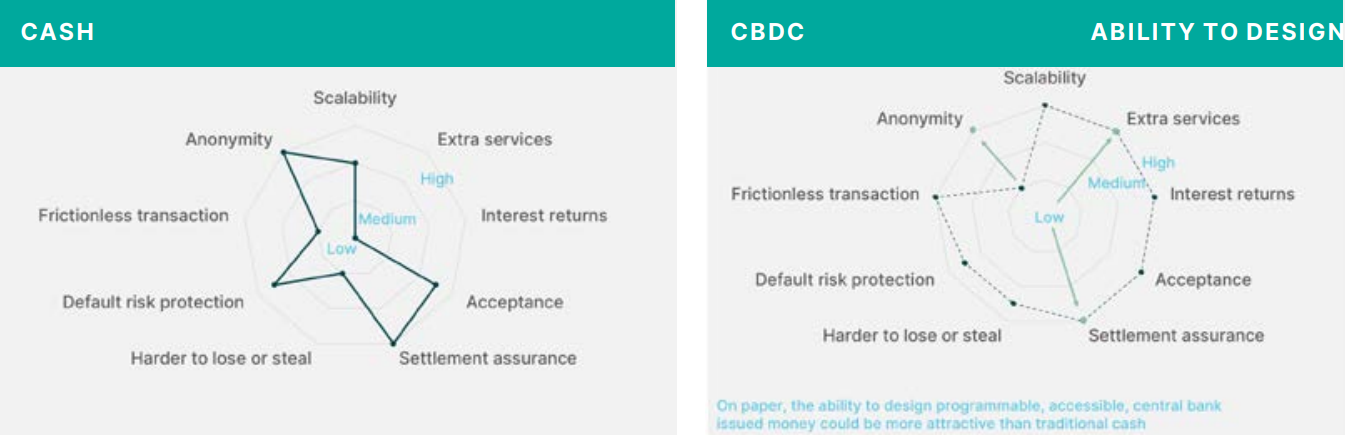

The IMF tried to depict the difference between different types of money in the form of a "radar chart":

Radar charts depicting the attractiveness of different forms of money and payment systems Source: The Block, IMF

Types of CBDC

There is no single generally accepted classification of CBDC. The key parameters by which you can divide them into types are:

- architecture

- infrastructure

- technology and conditions of access

- the level of anonymity

- the possibility of using for domestic and / or cross-border payments.

Architecture

According to the architecture, researchers distinguish two main categories of CBDC:

- Wholesale (they are Commercial or Direct)

- Retail (General purpose)

The retail category includes three types of architectures:

- Hybrid

- Intermediary

- Indirect (synthetic)

- architecture

- infrastructure

- technology and conditions of access

- the level of anonymity

- the possibility of using for domestic and / or cross-border payments.

Architecture

According to the architecture, researchers distinguish two main categories of CBDC:

- Wholesale (they are Commercial or Direct)

- Retail (General purpose)

The retail category includes three types of architectures:

- Hybrid

- Intermediary

- Indirect (synthetic)

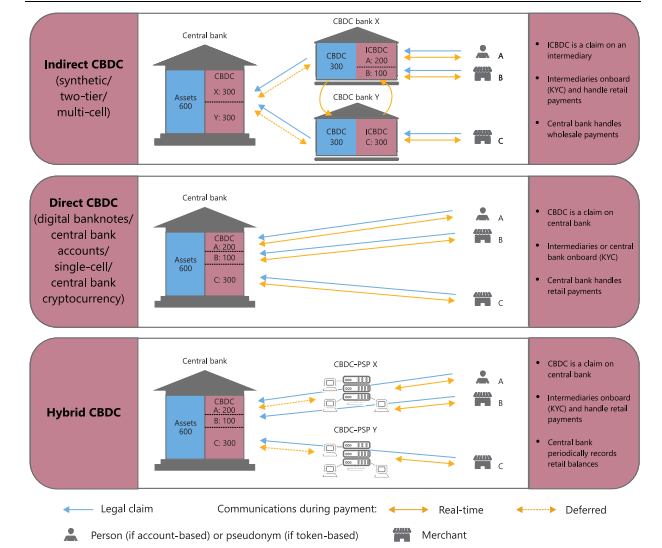

CBDC architectures. Data: BIS report from March 2020.

At the time of writing, four central banks are looking at a direct model (motive - increased financial inclusion)

seven consider a hybrid or intermediary model (some of them alongside the direct model)

However, most regulators have not yet decided on the architecture

seven consider a hybrid or intermediary model (some of them alongside the direct model)

However, most regulators have not yet decided on the architecture

What is Wholesale or Commercial CBDC (W-CBDC)?

The wholesale version of CBDC is a payment system operated by central banks.

It is available only to a narrow circle of users (financial institutions that store funds in central bank accounts and professional market participants).

Analogues of wholesale digital currencies are correspondent accounts and bank deposits with central banks.

In the case of calculating interest income, wholesale CBDCs can be viewed as interest-bearing liabilities of the central bank.

According to the authors of the report, commercial CBDC is a further development of the existing practice, in which the central bank issues currency to a virtual account and gives access to it to banks, and those, in turn, distribute the currency further throughout the economy.

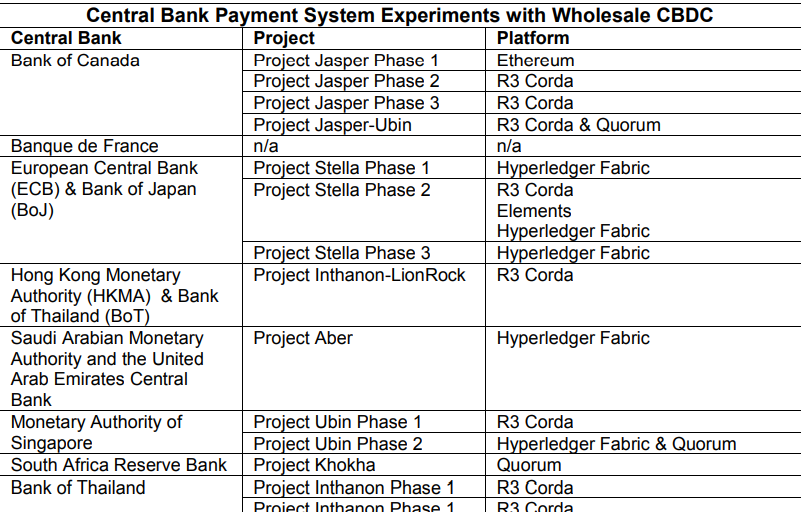

Among the main experiments of the W-CBDC, researchers noted the project of the ECB and the Bank of Japan (Project Stella), the Bank of Canada (Project Jasper), the Monetary Authority of Singapore (Project Ubin), as well as Hong Kong and Thailand.

It is available only to a narrow circle of users (financial institutions that store funds in central bank accounts and professional market participants).

Analogues of wholesale digital currencies are correspondent accounts and bank deposits with central banks.

In the case of calculating interest income, wholesale CBDCs can be viewed as interest-bearing liabilities of the central bank.

According to the authors of the report, commercial CBDC is a further development of the existing practice, in which the central bank issues currency to a virtual account and gives access to it to banks, and those, in turn, distribute the currency further throughout the economy.

Among the main experiments of the W-CBDC, researchers noted the project of the ECB and the Bank of Japan (Project Stella), the Bank of Canada (Project Jasper), the Monetary Authority of Singapore (Project Ubin), as well as Hong Kong and Thailand.

source: https://www.imf.org/en/Publications/WP/Issues/2020/06/26/A-Survey-of-Research-on-Retail-Central-Bank-Digital-Currency-49517

In all cases, W-CBDC testing was carried out using popular enterprise blockchain platforms:

R3 Corda, Quorum or Hyperledger Fabric.

Although blockchain is considered by some to be an optional technology for CBDC.

It was in the European-Japanese Project Stella that "anonymity vouchers" were used.

These are special electronic certificates that a platform participant could receive.

Transactions with attached "vouchers of anonymity" could go through without confirmation from the ECB:

The sender only had to indicate the amount, recipient ID and activate the anonymization function

(the voucher used in this case "burned out").

In this scenario, the identities of the participants in the translation were not verified.

Advantages of wholesale digital currencies

- the ability to regulate the demand for money;

- pursuing a flexible monetary policy;

- ensuring financial stability;

- provision of round-the-clock banking liquidity;

- reduction of costs for cross-border transfers;

- fixing transfers in a distributed ledger

- this increases the efficiency of settlements, as well as reduces credit and settlement risks,

since the source of funds and the guarantor of obligations is the central bank;

- reduction of counterparty risks

- pursuing a flexible monetary policy;

- ensuring financial stability;

- provision of round-the-clock banking liquidity;

- reduction of costs for cross-border transfers;

- fixing transfers in a distributed ledger

- this increases the efficiency of settlements, as well as reduces credit and settlement risks,

since the source of funds and the guarantor of obligations is the central bank;

- reduction of counterparty risks

Disadvantages of wholesale digital currencies

- the scope of distribution is limited to interbank transactions, settlements on transfers, clearing operations and international trade

(where banks often act as guarantors for transactions).

(where banks often act as guarantors for transactions).

Implementation perspective

The wholesale CBDC model is the most popular among central banks because it has the potential to speed up the operation of financial systems, increase their security and reduce costs.

In developed countries, retail payment and settlement systems are already quite efficient, operate almost in real time and are always available. Most citizens have access to banking services.

Wholesale CBDC technology will increase the efficiency of interaction between different areas.

Direct linking of stock or foreign exchange platforms to cash platforms can improve the speed of transactions and eliminate settlement risk. The speed of transactions in the OTC markets and in the areas of syndicated lending, as well as settlements for international trade transactions, can significantly increase when establishing a connection with the instant settlement system based on wholesale CBDC.

Also, wholesale CBDCs can simplify the cross-border payment infrastructure by significantly reducing the number of intermediaries.

This will increase its efficiency and safety, reduce costs, and reduce liquidity and counterparty risks.

The introduction of distributed ledger technology will also make it possible to give wholesale CBDCs the characteristics of “smart”, including targeted financing, limiting their use in time and space, and applying conditional interest rates.

These features will allow central banks to leverage new monetary policy instruments such as personal lending rates.

Real-time monitoring and tracking options, as well as control over the money supply, will help banks and regulators in the fight against money laundering and in supervision.

In developed countries, retail payment and settlement systems are already quite efficient, operate almost in real time and are always available. Most citizens have access to banking services.

Wholesale CBDC technology will increase the efficiency of interaction between different areas.

Direct linking of stock or foreign exchange platforms to cash platforms can improve the speed of transactions and eliminate settlement risk. The speed of transactions in the OTC markets and in the areas of syndicated lending, as well as settlements for international trade transactions, can significantly increase when establishing a connection with the instant settlement system based on wholesale CBDC.

Also, wholesale CBDCs can simplify the cross-border payment infrastructure by significantly reducing the number of intermediaries.

This will increase its efficiency and safety, reduce costs, and reduce liquidity and counterparty risks.

The introduction of distributed ledger technology will also make it possible to give wholesale CBDCs the characteristics of “smart”, including targeted financing, limiting their use in time and space, and applying conditional interest rates.

These features will allow central banks to leverage new monetary policy instruments such as personal lending rates.

Real-time monitoring and tracking options, as well as control over the money supply, will help banks and regulators in the fight against money laundering and in supervision.

What are retail CBDC?

Retail CBDCs are digital currencies available for widespread use by individuals and legal entities.

Serves as a replacement for cash (or a supplement) and an alternative to bank deposits. Accrual of interest income, as a rule, is not provided.

Serves as a replacement for cash (or a supplement) and an alternative to bank deposits. Accrual of interest income, as a rule, is not provided.

Key features of retail CBDCs

While there are many variations on the retail digital currency model, most central banks highlight the following key characteristics:

- Retail CBDC should be a new form of central bank money issued and controlled by the regulator.

The retail digital currency supply is driven by monetary policy and controlled by the central bank.

- CBDC should be included in the financial statements of the central bank.

- Digital currency should be accepted as a means of payment by all citizens, companies and government bodies.

- CBDC is distributed by the central bank on a one-to-one basis with fiat currency and must be freely convertible into cash.

- CBDCs should operate on an open infrastructure, which will allow private companies to create new products and services.

- The transaction cost should be less than in existing systems.

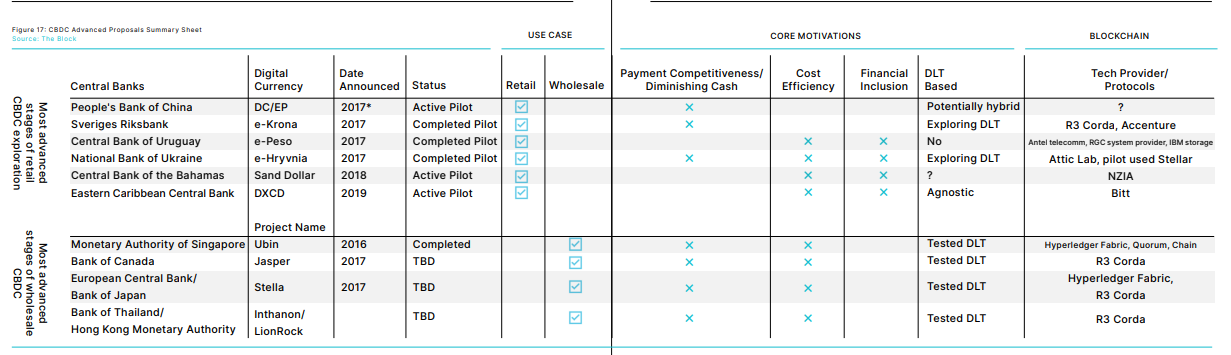

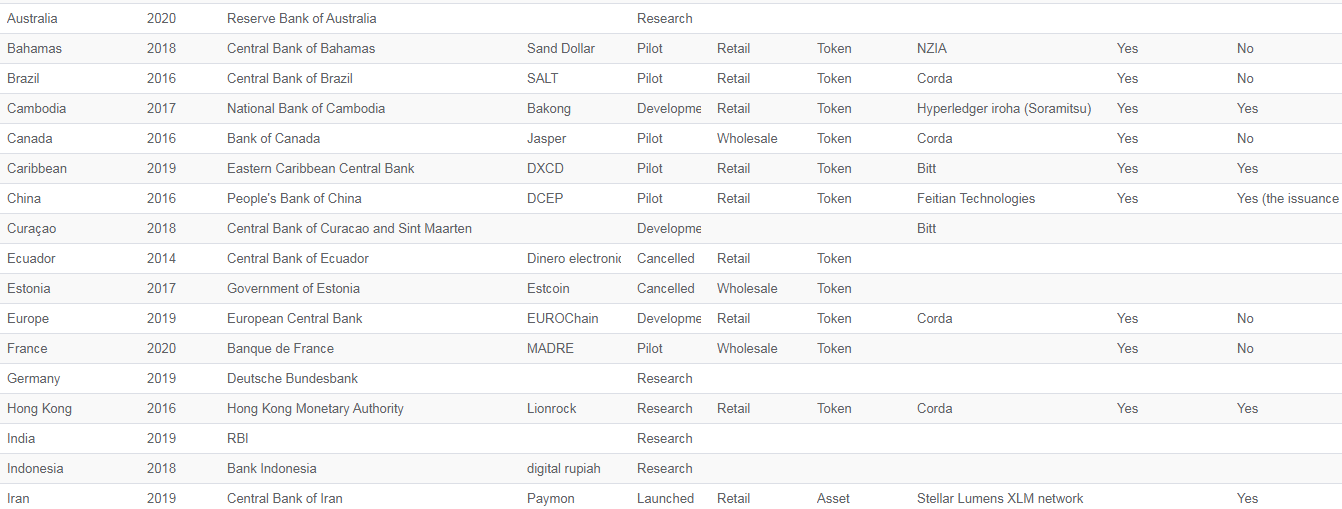

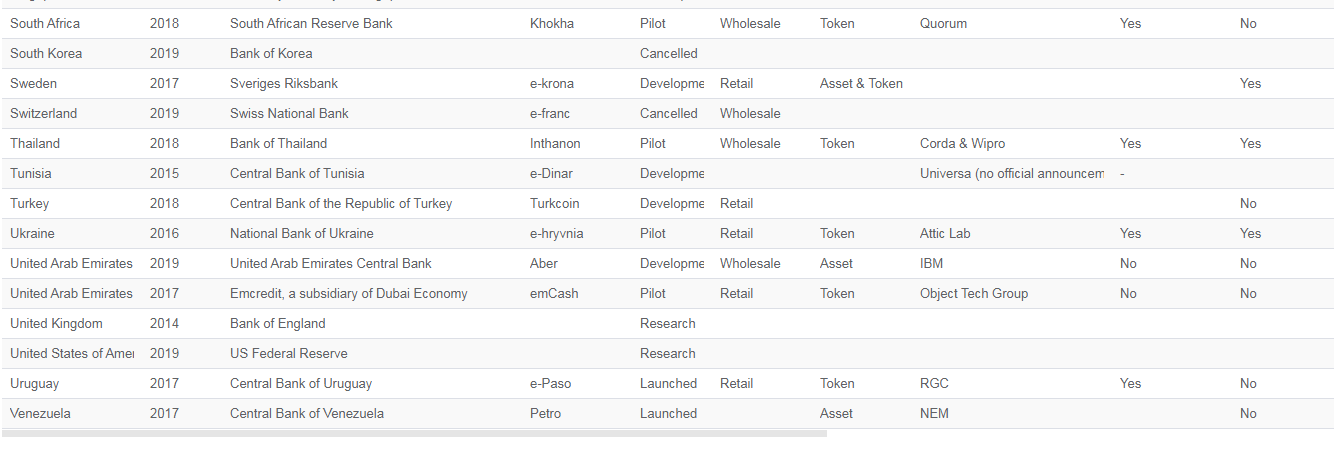

The most notable experiments with CBDC are seen in the following countries:

- Retail CBDC should be a new form of central bank money issued and controlled by the regulator.

The retail digital currency supply is driven by monetary policy and controlled by the central bank.

- CBDC should be included in the financial statements of the central bank.

- Digital currency should be accepted as a means of payment by all citizens, companies and government bodies.

- CBDC is distributed by the central bank on a one-to-one basis with fiat currency and must be freely convertible into cash.

- CBDCs should operate on an open infrastructure, which will allow private companies to create new products and services.

- The transaction cost should be less than in existing systems.

The most notable experiments with CBDC are seen in the following countries:

Although the "commercial" CBDC is considered as a safer option for the stability of the financial system,

for mass users it is the "retail" CBDC that is of interest

..A full-fledged replacement for regular currency, which can be used to pay for goods and services, stored in a bank account, etc.

Sweden became one of the first countries whose authorities thought about CBDC.

The reason is the extremely low use of cash (they accounted for only 5% of all household payments, while 60% were paid with bank cards). Testing of the "digital crown" (e-krona) began in 2017 (information about the plans appeared in the media a year earlier).

After three years of study, they entered the pilot stage.

In the development of CBDC, the regulator is assisted by Accenture - it is responsible for payments, deposits, transfers and other functions on the R3 Corda blockchain.

Uruguay, one of the most economically prosperous countries in Latin America, piloted its own CBDC (e-peso) from September 2017 to April 2018 among consumers and businesses.

Instead of a distributed ledger, digital wallets operated by the state telecommunications company Antel operated.

At the same time, the e-peso system provided for anonymous transactions and transfers without an Internet connection, and each e-peso “banknote” had a unique cryptographic signature.

Now the results of the project are being assessed in terms of the feasibility of user anonymity, the possibility of introducing “interest rate” instruments and the overall impact on the economy.

According to the study, Ukraine has become another European country that is actively developing "retail" CBDC.

The National Bank of Ukraine (NBU) successfully tested the "digital hryvnia" during four months of 2018.

During the test, the NBU "released" 5443 electronic hryvnia, which were used on 79 wallets on smartphones.

Wallets could be additionally replenished through the Ukrainian Payment Space payment system integrated into the CBDC platform.

Users could transfer digital money between wallets, replenish the balance of mobile numbers of the LifeCell operator and make charitable donations.

The platform itself was built on a private version of the Stellar protocol and had two levels:

in the first, the NBU unilaterally managed the register, in the second, banks and financial institutions managed operations.

As a result, Stellar was deemed unsuitable for a nationwide system, but no alternative has yet been named.

Now the Ukrainian central bank is studying both a centralized and a decentralized model of the digital hryvnia system.

Summing up the experiment at the CBDC conference in February this year, the then head of the NBU, Yakov Smoliy, said:

"We continue to explore the possibility of issuing a digital hryvnia and will return to this issue when we are confident that the initiative is technically feasible and that the digital currency will not interfere with the central bank's performance of its functions to ensure the exchange rate and financial stability."

for mass users it is the "retail" CBDC that is of interest

..A full-fledged replacement for regular currency, which can be used to pay for goods and services, stored in a bank account, etc.

Sweden became one of the first countries whose authorities thought about CBDC.

The reason is the extremely low use of cash (they accounted for only 5% of all household payments, while 60% were paid with bank cards). Testing of the "digital crown" (e-krona) began in 2017 (information about the plans appeared in the media a year earlier).

After three years of study, they entered the pilot stage.

In the development of CBDC, the regulator is assisted by Accenture - it is responsible for payments, deposits, transfers and other functions on the R3 Corda blockchain.

Uruguay, one of the most economically prosperous countries in Latin America, piloted its own CBDC (e-peso) from September 2017 to April 2018 among consumers and businesses.

Instead of a distributed ledger, digital wallets operated by the state telecommunications company Antel operated.

At the same time, the e-peso system provided for anonymous transactions and transfers without an Internet connection, and each e-peso “banknote” had a unique cryptographic signature.

Now the results of the project are being assessed in terms of the feasibility of user anonymity, the possibility of introducing “interest rate” instruments and the overall impact on the economy.

According to the study, Ukraine has become another European country that is actively developing "retail" CBDC.

The National Bank of Ukraine (NBU) successfully tested the "digital hryvnia" during four months of 2018.

During the test, the NBU "released" 5443 electronic hryvnia, which were used on 79 wallets on smartphones.

Wallets could be additionally replenished through the Ukrainian Payment Space payment system integrated into the CBDC platform.

Users could transfer digital money between wallets, replenish the balance of mobile numbers of the LifeCell operator and make charitable donations.

The platform itself was built on a private version of the Stellar protocol and had two levels:

in the first, the NBU unilaterally managed the register, in the second, banks and financial institutions managed operations.

As a result, Stellar was deemed unsuitable for a nationwide system, but no alternative has yet been named.

Now the Ukrainian central bank is studying both a centralized and a decentralized model of the digital hryvnia system.

Summing up the experiment at the CBDC conference in February this year, the then head of the NBU, Yakov Smoliy, said:

"We continue to explore the possibility of issuing a digital hryvnia and will return to this issue when we are confident that the initiative is technically feasible and that the digital currency will not interfere with the central bank's performance of its functions to ensure the exchange rate and financial stability."

Implementation perspective

The retail CBDC concept is comparatively popular among emerging economies' central banks, where financial institutions are seeking to lead the rapidly growing fintech industry, promote financial inclusion by accelerating the movement towards a cashless society, and reduce the cost of issuing money and processing banknotes.

Central banks in developed countries are not very enthusiastic about retail CBDCs.

Regulators are unwilling to create competition between central bank funds and the private sector, considering the potential benefits of using retail digital currencies to be limited.

In their opinion, introducing retail CDBCs is too bold (or premature).

What are Hybrid CBDC?

Hybrid digital currencies are a cross between direct (wholesale) and indirect (synthetic) CBDCs.

Payment processing is handled by intermediaries, but the digital currency itself is a direct payment request to the central bank.

The latter is responsible for a distributed ledger with all transactions and manages a back-up technical infrastructure that allows the payment system to be restarted in the event of a failure.

One of the key elements of the hybrid CBDC architecture is the legal and regulatory framework that underpins currency rights, separating them from the balance sheets of the payment service provider (PSP).

If the supplier is unable to meet its obligations, then the assets held in the CBDC are not considered part of the PSP's assets available to lenders.

The legal framework gives the central bank the ability to transfer a retail customer's contract with an unworkable PSP to a fully functional provider.

Another key element is the technical ability to transfer assets.

The bank is obliged to support the payment process in a situation where the intermediary is experiencing technical difficulties.

Therefore, the financial institution needs the ability to restore the balance of a retail client.

Therefore, the bank retains a copy of the retail customer's CBDC assets, which allows assets to be moved from one PSP to another in the event of a technical failure.

Payment processing is handled by intermediaries, but the digital currency itself is a direct payment request to the central bank.

The latter is responsible for a distributed ledger with all transactions and manages a back-up technical infrastructure that allows the payment system to be restarted in the event of a failure.

One of the key elements of the hybrid CBDC architecture is the legal and regulatory framework that underpins currency rights, separating them from the balance sheets of the payment service provider (PSP).

If the supplier is unable to meet its obligations, then the assets held in the CBDC are not considered part of the PSP's assets available to lenders.

The legal framework gives the central bank the ability to transfer a retail customer's contract with an unworkable PSP to a fully functional provider.

Another key element is the technical ability to transfer assets.

The bank is obliged to support the payment process in a situation where the intermediary is experiencing technical difficulties.

Therefore, the financial institution needs the ability to restore the balance of a retail client.

Therefore, the bank retains a copy of the retail customer's CBDC assets, which allows assets to be moved from one PSP to another in the event of a technical failure.

Pros and cons of hybrid CBDC

As an intermediate solution, this model may have better stress tolerance than indirect (synthetic) CBDCs, but more complex in infrastructure management from the point of view of the central bank.

Hybrid CBDCs are somewhat easier to manage than direct (bulk) ones.

Since the central bank does not interact directly with retail users, it can focus on a limited set of key processes, such as settlement of payments. At the same time, intermediaries can manage other services, including confirmation of instant payments.

Hybrid CBDCs enhance central bank reserve storage capabilities and improve interoperability between different payment systems.

Hybrid CBDCs are somewhat easier to manage than direct (bulk) ones.

Since the central bank does not interact directly with retail users, it can focus on a limited set of key processes, such as settlement of payments. At the same time, intermediaries can manage other services, including confirmation of instant payments.

Hybrid CBDCs enhance central bank reserve storage capabilities and improve interoperability between different payment systems.

What are intermediary CBDC?

The architecture of intermediary digital currencies resembles that of hybrid CBDCs.

In this case, the monetary regulator controls the wholesale register, not the central register of all retail transactions.

Intermediary CBDCs represent a direct payment claim against the central bank, while payments are made by intermediaries.

The Bank for International Settlements (BIS) notes an increase in the number of central banks that are leaning towards hybrid and intermediary CBDC models.

Only a few jurisdictions are considering “direct” projects, in which the regulator takes over all user payments.

In this case, the monetary regulator controls the wholesale register, not the central register of all retail transactions.

Intermediary CBDCs represent a direct payment claim against the central bank, while payments are made by intermediaries.

The Bank for International Settlements (BIS) notes an increase in the number of central banks that are leaning towards hybrid and intermediary CBDC models.

Only a few jurisdictions are considering “direct” projects, in which the regulator takes over all user payments.

What are synthetic or indirect CBDC (sCBDC)?

Along with the above three general purpose CBDC architectures, there is another approach.

It is based on a model for the indirect provision of retail digital currencies through financial intermediaries.

The sCBDC model is also known as “two-tier” CBDC because it resembles the existing two-tier banking system.

Issuing intermediaries secure all of the regulator's obligations to retail customers (in the form of indirect CBDCs) through assets in actual CBDCs (or other funds) deposited with the central bank.

Intermediaries control communications with retail customers, online payments and messages to other intermediaries, and bulk payment instructions to the central bank.

Central banks protect the assets and rights of intermediate clients (issuing companies), monitor the ledger of transactions, and manage the backup technical infrastructure.

The sCBDCs issued by intermediary companies are backed by central bank reserves.

sCBDCs demand increased access to central bank reserves for financial institutions, fintech startups, and large technology companies.

Back-up collateral allows sCBDC providers to guarantee repayment at par.

It is based on a model for the indirect provision of retail digital currencies through financial intermediaries.

The sCBDC model is also known as “two-tier” CBDC because it resembles the existing two-tier banking system.

Issuing intermediaries secure all of the regulator's obligations to retail customers (in the form of indirect CBDCs) through assets in actual CBDCs (or other funds) deposited with the central bank.

Intermediaries control communications with retail customers, online payments and messages to other intermediaries, and bulk payment instructions to the central bank.

Central banks protect the assets and rights of intermediate clients (issuing companies), monitor the ledger of transactions, and manage the backup technical infrastructure.

The sCBDCs issued by intermediary companies are backed by central bank reserves.

sCBDCs demand increased access to central bank reserves for financial institutions, fintech startups, and large technology companies.

Back-up collateral allows sCBDC providers to guarantee repayment at par.

Pros and cons of sCBDC

sCBDCs are cheaper and less risky compared to direct-produced and more manageable counterparts.

They also enable the private sector to innovate and engage with customers more effectively, and central banks to build trust with users.

The downside is that society can view sCBDC as a product released under the brand of a central bank, not fully realizing that the regulator has limited responsibility for it.

They also enable the private sector to innovate and engage with customers more effectively, and central banks to build trust with users.

The downside is that society can view sCBDC as a product released under the brand of a central bank, not fully realizing that the regulator has limited responsibility for it.

How do central banks view CBDC?

According to experts, the CBDC development is one of the most important trends in the monetary sphere, which will radically change the world of money in the next decade.

As of January 2020 more than 80% of central banks were engaged in CBDC research and development.

As of January 2020 more than 80% of central banks were engaged in CBDC research and development.

Source Data: blog ConsenSys

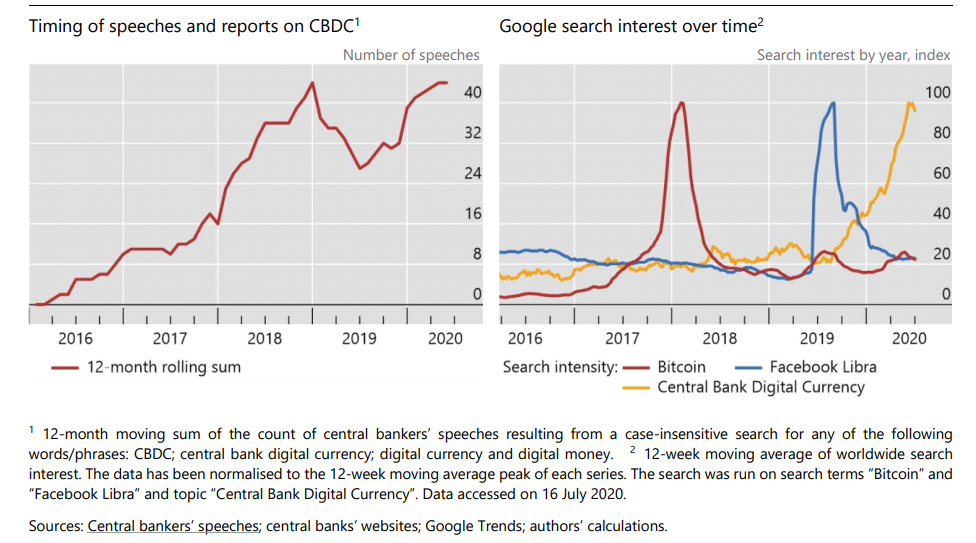

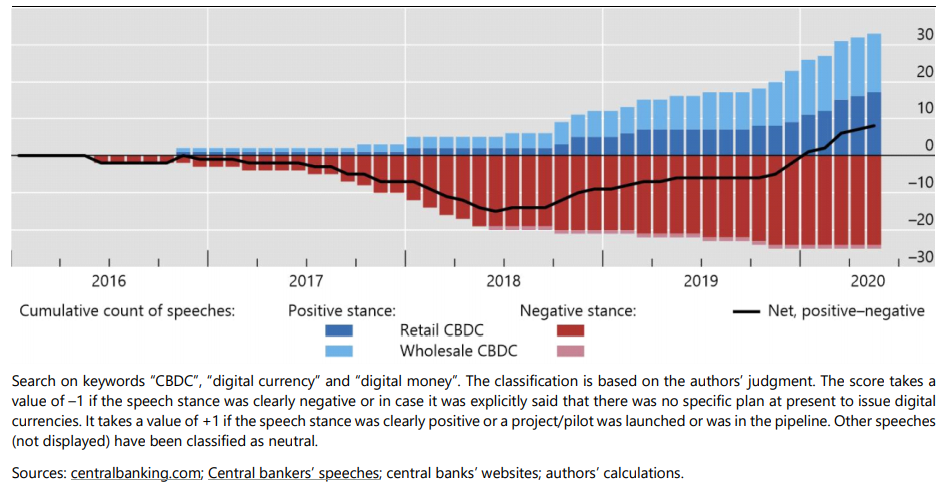

A report released by the BIS in April 2020 shows that the Coronavirus pandemic has only accelerated development in this direction.

According to the document, China, Sweden and Canada are leading the CBDC development.

Compared to 2019, the number of speeches in which representatives of central banks touched upon various aspects of CBDC has increased.

According to the document, China, Sweden and Canada are leading the CBDC development.

Compared to 2019, the number of speeches in which representatives of central banks touched upon various aspects of CBDC has increased.

Source Data: report BIS from August 2020. https://www.bis.org/publ/work880.pdf

If in 2017-2018 public statements by managers and board members of central banks about digital currencies were predominantly negative, especially with respect to retail CBDCs, then at the end of 2018 the rhetoric began to change.

Currently, representatives of central banks assess CBDC rather positively.

Currently, representatives of central banks assess CBDC rather positively.

Data: report BIS from August 2020.

The number of central banks ready to issue CBDC in the next six years has doubled in 2019:

Central banks, representing a fifth of the world's population, have indicated that they are likely to release CBDC in the near future.

As of mid-July 2020, 36 central banks have published papers looking at retail or wholesale CBDCs.

At least three countries (Uruguay, Ecuador and Ukraine) have completed pilot retail CBDC projects.

Six more retail CBDCs are currently being piloted in Sweden, South Korea, the Eastern Caribbean Monetary Union, the Bahamas, the PRC and Cambodia.

Central banks, representing a fifth of the world's population, have indicated that they are likely to release CBDC in the near future.

As of mid-July 2020, 36 central banks have published papers looking at retail or wholesale CBDCs.

At least three countries (Uruguay, Ecuador and Ukraine) have completed pilot retail CBDC projects.

Six more retail CBDCs are currently being piloted in Sweden, South Korea, the Eastern Caribbean Monetary Union, the Bahamas, the PRC and Cambodia.

Data: report BIS from August 2020.

What CBDCs do central banks study and test?

- Architecture

A growing number of banks are considering promising digital currencies with hybrid or intermediary architectures. In this context, CBDC is a direct payment request to the central bank, but the private sector controls interactions with customers.

Only a few jurisdictions are considering models in which the central bank plays a significant operational role in payments to customers. Central banks are more likely to choose direct or hybrid / intermediary architectures in jurisdictions with a relatively high standard of living, broad public access to banking services, and effective governance. In less developed countries, central banks generally do not specify the architecture they choose.

- Infrastructure (technical concept) CBDC

The infrastructure can be based on either a traditional centralized database or a distributed ledger (DLT).

Many banks are considering various technology options. However, the current approbation of the CBDC concept is based primarily on DLT rather than traditional technology infrastructure. Central banks experimenting with DLT use, as a rule, permissioned systems, in which operators have the right to decide who to admit to the network.

- Access technology and degree of anonymity of use:

- account-based

Account-based CBDCs are tied to identity information. Combining the qualities of cash as an inclusive and crisis-resistant means of payment with the characteristics of anonymity can be challenging. This is the most popular concept - five central banks are considering it.

- token-based

The access mechanism based on digital tokens allows implementing various value-based payment options - for example, issuing prepaid CBDC banknotes. The latter can be exchanged both physically and digitally.

However, this comes with the risk of criminal activity and counterfeiting. In addition, access under such a scheme is difficult for people without access to banking services and forced to use only cash, a concept that three central banks are considering.

- Can be used for domestic and / or cross-border payments

CBDCs can be used for domestic settlements or for cross-border payments. Accordingly, a digital currency model can provide retail and wholesale relationships and access options for residents or non-residents. The token-based internal CBDC will be open to everyone, including non-residents.

Most projects tend to be used internally. The ECB, the central banks of France, Spain, the Netherlands, and the Eastern Caribbean Central Bank, by contrast, are focusing on the cross-border use of digital currencies.

A growing number of banks are considering promising digital currencies with hybrid or intermediary architectures. In this context, CBDC is a direct payment request to the central bank, but the private sector controls interactions with customers.

Only a few jurisdictions are considering models in which the central bank plays a significant operational role in payments to customers. Central banks are more likely to choose direct or hybrid / intermediary architectures in jurisdictions with a relatively high standard of living, broad public access to banking services, and effective governance. In less developed countries, central banks generally do not specify the architecture they choose.

- Infrastructure (technical concept) CBDC

The infrastructure can be based on either a traditional centralized database or a distributed ledger (DLT).

Many banks are considering various technology options. However, the current approbation of the CBDC concept is based primarily on DLT rather than traditional technology infrastructure. Central banks experimenting with DLT use, as a rule, permissioned systems, in which operators have the right to decide who to admit to the network.

- Access technology and degree of anonymity of use:

- account-based

Account-based CBDCs are tied to identity information. Combining the qualities of cash as an inclusive and crisis-resistant means of payment with the characteristics of anonymity can be challenging. This is the most popular concept - five central banks are considering it.

- token-based

The access mechanism based on digital tokens allows implementing various value-based payment options - for example, issuing prepaid CBDC banknotes. The latter can be exchanged both physically and digitally.

However, this comes with the risk of criminal activity and counterfeiting. In addition, access under such a scheme is difficult for people without access to banking services and forced to use only cash, a concept that three central banks are considering.

- Can be used for domestic and / or cross-border payments

CBDCs can be used for domestic settlements or for cross-border payments. Accordingly, a digital currency model can provide retail and wholesale relationships and access options for residents or non-residents. The token-based internal CBDC will be open to everyone, including non-residents.

Most projects tend to be used internally. The ECB, the central banks of France, Spain, the Netherlands, and the Eastern Caribbean Central Bank, by contrast, are focusing on the cross-border use of digital currencies.

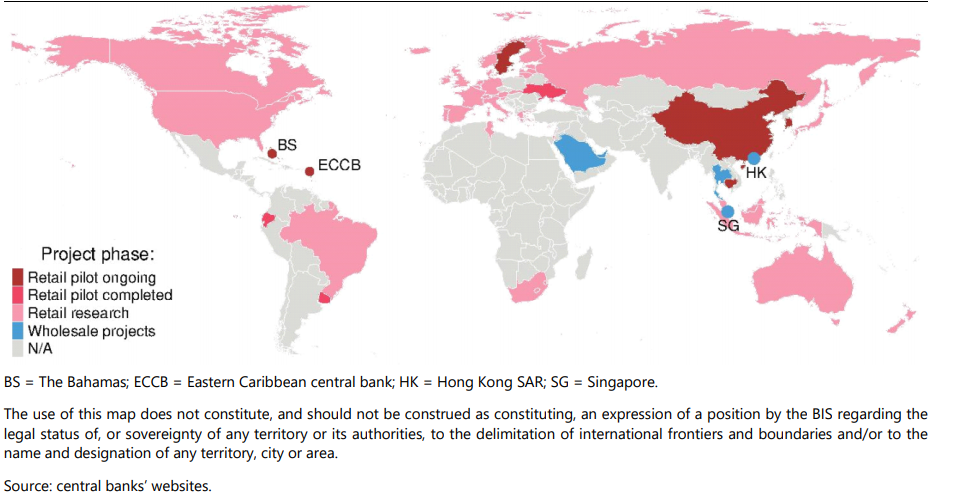

CBDC Tracker

CBDC Tracker - here is a world map showing the countries involved in one way or another in the development of the CBDC.

World CBDC Race

- The Bank of Canada has opened a vacancy for a digital currency economist.

https://careers.bankofcanada.ca/job/Ottawa-%28Downtown%29-Economist%2C-Digital-Currencies-and-Financial-Technologies-ON/542179017/

The regulator called on other countries to coordinate development approaches.

https://careers.bankofcanada.ca/job/Ottawa-%28Downtown%29-Economist%2C-Digital-Currencies-and-Financial-Technologies-ON/542179017/

- The ECB applied for the registration of the digital euro trademark and published a report on a possible digital euro issue.

https://euipo.europa.eu/eSearch/#basic/1+1+1+1/100+100+100+100/digital%20euro

https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf

Then the ECB named the main use cases for CBDC.

https://www.bis.org/review/r201022f.pdf

- Bank of Korea will launch the last round of digital won testing in 2021.

http://www.koreaherald.com/view.php?ud=20201007000809

- Bank of Switzerland and BIS will start testing CBDC.

https://www.theblockcrypto.com/linked/82299/swiss-central-bank-bis-digital-currency-test

- The Bank of Japan said that the public will determine the feasibility of developing a digital currency.

https://www.bnnbloomberg.ca/boj-official-says-digital-currency-needs-public-support-first-1.1512038

- The first distribution of the digital yuan took place in China.

https://www.scmp.com/business/banking-finance/article/3104281/peoples-bank-chinas-digital-currency-already-used-pilot

https://www.bloomberg.com/news/articles/2020-11-02/pboc-governor-says-4-million-transactions-so-far-in-digital-yuan?sref=naTJVz8t

- Central Bank of New Zealand reported on research in the field of CBDC.

https://www.bis.org/review/r190527b.htm

- The Central Bank of Kenya is considering the release of the CBDC.

https://kenyanwallstreet.com/cbk-in-discussions-over-digital-currency/

https://careers.bankofcanada.ca/job/Ottawa-%28Downtown%29-Economist%2C-Digital-Currencies-and-Financial-Technologies-ON/542179017/

The regulator called on other countries to coordinate development approaches.

https://careers.bankofcanada.ca/job/Ottawa-%28Downtown%29-Economist%2C-Digital-Currencies-and-Financial-Technologies-ON/542179017/

- The ECB applied for the registration of the digital euro trademark and published a report on a possible digital euro issue.

https://euipo.europa.eu/eSearch/#basic/1+1+1+1/100+100+100+100/digital%20euro

https://www.ecb.europa.eu/pub/pdf/other/Report_on_a_digital_euro~4d7268b458.en.pdf

Then the ECB named the main use cases for CBDC.

https://www.bis.org/review/r201022f.pdf

- Bank of Korea will launch the last round of digital won testing in 2021.

http://www.koreaherald.com/view.php?ud=20201007000809

- Bank of Switzerland and BIS will start testing CBDC.

https://www.theblockcrypto.com/linked/82299/swiss-central-bank-bis-digital-currency-test

- The Bank of Japan said that the public will determine the feasibility of developing a digital currency.

https://www.bnnbloomberg.ca/boj-official-says-digital-currency-needs-public-support-first-1.1512038

- The first distribution of the digital yuan took place in China.

https://www.scmp.com/business/banking-finance/article/3104281/peoples-bank-chinas-digital-currency-already-used-pilot

https://www.bloomberg.com/news/articles/2020-11-02/pboc-governor-says-4-million-transactions-so-far-in-digital-yuan?sref=naTJVz8t

- Central Bank of New Zealand reported on research in the field of CBDC.

https://www.bis.org/review/r190527b.htm

- The Central Bank of Kenya is considering the release of the CBDC.

https://kenyanwallstreet.com/cbk-in-discussions-over-digital-currency/

China leads the CBDC race with DCEP

Perhaps the most attention is now riveted to what the digital currency of the world's second economy will be like.

According to The Block report, the first work on the "digital yuan"

(officially called Digital Currency, Electronic Payment, or DCEP)

.......started back in 2014.

- The first report of the People's Bank of China in early October reported the successful processing of 3.13 million transactions for 1.1 billion yuan (~ $ 162 million) in digital yuan (DCEP).

By the end of the month, it had processed over 4 million transactions worth over 2 billion yuan (~ $ 299 million).

This is still a test phase.

https://www.scmp.com/business/banking-finance/article/3104281/peoples-bank-chinas-digital-currency-already-used-pilot

https://www.bloomberg.com/news/articles/2020-11-02/pboc-governor-says-4-million-transactions-so-far-in-digital-yuan?sref=naTJVz8t

- On October 8, the Shenzhen authorities announced the first distribution of digital currency to 50,000 residents of Luohu District, which attracted almost 2 million people.

50,000 participants of the bounty program received 200 yuan (~ $ 29.5) each, they had to be spent from October 12 to 18 in 3389 outlets.

https://twitter.com/chinadefi1/status/1314253720935227392?ref_src=twsrc%5Etfw

https://www.asiaone.com/money/shenzhens-2m-digital-currency-lottery-attracts-2-million-hopefuls

- As part of the pilot project, 11 gas stations in Shenzhen have implemented support for the digital yuan.

https://decrypt.co/45254/digital-yuan-rolls-out-for-use-in-shenzhen-gas-stations

- 47,573 out of 50,000 lottery winners (95%) spent the intended funds, making 62,788 transactions worth 8.8 million yuan (~ $ 1.3 million).

https://cointelegraph.com/news/95-of-winners-in-china-s-cbdc-lottery-spent-digital-yuan-prizes

- In October, information appeared about the readiness for testing in the digital yuan of the functions of "offline payments" and the limited anonymity of transactions, when the merchant is not reflected in the record.

At the end of the month, Huawei announced the implementation of DCEP support in the hardware wallet built into the Mate 40 smartphone, which will also allow offline payments.

https://news.8btc.com/dual-offline-wallet-for-chinas-cbdc-is-ready-for-test

https://news.8btc.com/chinese-digital-yuan-is-testing-limited-anonymous-transaction

https://www.theblockcrypto.com/linked/82985/huawei-hardware-wallet-china-digital-yuan

- The Central Bank of China announced the emergence of fake digital yuan wallets and amended legislation to combat the issuance of DCEP-based tokens.

https://news.8btc.com/china-is-already-seeing-fakes-of-its-still-developing-digital-yuan-wallet

https://twitter.com/WuBlockchain

Judging by the ongoing experiment, the digital yuan will become a full-fledged replacement for cash.

There are all conditions for this:

China today is the largest market for mobile payments with over a billion users.

According to The Block's report, the central bank will oversee the issue, the main registry and issues of anonymity, while commercial banks will serve as wallet providers and infrastructure for operations.

The Chinese authorities want to bring digital currency closer to cash in terms of anonymity, as can be seen from the patents registered by the People's Bank of China.

DCEP is planning to incorporate "controlled anonymity" into its architecture.

This means that different participants in the system will have limited information about each other.

However, government agencies can easily obtain the data they need.

Offline transactions should become another characteristic of the “cash” of the digital yuan.

Chuanwei analyst David Zu gave his forecast on the development of the Chinese CBDC to the authors of the report.

According to him, the experiment using DCEP in retail will continue

(it has already been extended to six cities):

"I think more uses will be tried as the People's Bank of China wants to test the strength of the chosen system design, as well as examine the user experience and potential risks."

In a year, the Chinese authorities must determine a strategy for bringing DCEP to the market, the expert believes.

In addition to domestic use, China may use the digital yuan to squeeze out the US dollar, which dominates international transactions.

For this DCEP must, in particular, become a competitor to SWIFT.

In addition, as former IMF chief economist Kenneth Rogoff argued, one of the directions of the digital yuan's expansion abroad is the underground market.

The 2022 Winter Olympics could be a likely field for DCEP testing in foreign audiences.

As for the largest economy, the United States,

The Block says the Fed is still taking a "conservative approach" towards CBDCs.

According to The Block report, the first work on the "digital yuan"

(officially called Digital Currency, Electronic Payment, or DCEP)

.......started back in 2014.

- The first report of the People's Bank of China in early October reported the successful processing of 3.13 million transactions for 1.1 billion yuan (~ $ 162 million) in digital yuan (DCEP).

By the end of the month, it had processed over 4 million transactions worth over 2 billion yuan (~ $ 299 million).

This is still a test phase.

https://www.scmp.com/business/banking-finance/article/3104281/peoples-bank-chinas-digital-currency-already-used-pilot

https://www.bloomberg.com/news/articles/2020-11-02/pboc-governor-says-4-million-transactions-so-far-in-digital-yuan?sref=naTJVz8t

- On October 8, the Shenzhen authorities announced the first distribution of digital currency to 50,000 residents of Luohu District, which attracted almost 2 million people.

50,000 participants of the bounty program received 200 yuan (~ $ 29.5) each, they had to be spent from October 12 to 18 in 3389 outlets.

https://twitter.com/chinadefi1/status/1314253720935227392?ref_src=twsrc%5Etfw

https://www.asiaone.com/money/shenzhens-2m-digital-currency-lottery-attracts-2-million-hopefuls

- As part of the pilot project, 11 gas stations in Shenzhen have implemented support for the digital yuan.

https://decrypt.co/45254/digital-yuan-rolls-out-for-use-in-shenzhen-gas-stations

- 47,573 out of 50,000 lottery winners (95%) spent the intended funds, making 62,788 transactions worth 8.8 million yuan (~ $ 1.3 million).

https://cointelegraph.com/news/95-of-winners-in-china-s-cbdc-lottery-spent-digital-yuan-prizes

- In October, information appeared about the readiness for testing in the digital yuan of the functions of "offline payments" and the limited anonymity of transactions, when the merchant is not reflected in the record.

At the end of the month, Huawei announced the implementation of DCEP support in the hardware wallet built into the Mate 40 smartphone, which will also allow offline payments.

https://news.8btc.com/dual-offline-wallet-for-chinas-cbdc-is-ready-for-test

https://news.8btc.com/chinese-digital-yuan-is-testing-limited-anonymous-transaction

https://www.theblockcrypto.com/linked/82985/huawei-hardware-wallet-china-digital-yuan

- The Central Bank of China announced the emergence of fake digital yuan wallets and amended legislation to combat the issuance of DCEP-based tokens.

https://news.8btc.com/china-is-already-seeing-fakes-of-its-still-developing-digital-yuan-wallet

https://twitter.com/WuBlockchain

Judging by the ongoing experiment, the digital yuan will become a full-fledged replacement for cash.

There are all conditions for this:

China today is the largest market for mobile payments with over a billion users.

According to The Block's report, the central bank will oversee the issue, the main registry and issues of anonymity, while commercial banks will serve as wallet providers and infrastructure for operations.

The Chinese authorities want to bring digital currency closer to cash in terms of anonymity, as can be seen from the patents registered by the People's Bank of China.

DCEP is planning to incorporate "controlled anonymity" into its architecture.

This means that different participants in the system will have limited information about each other.

However, government agencies can easily obtain the data they need.

Offline transactions should become another characteristic of the “cash” of the digital yuan.

Chuanwei analyst David Zu gave his forecast on the development of the Chinese CBDC to the authors of the report.

According to him, the experiment using DCEP in retail will continue

(it has already been extended to six cities):

"I think more uses will be tried as the People's Bank of China wants to test the strength of the chosen system design, as well as examine the user experience and potential risks."

In a year, the Chinese authorities must determine a strategy for bringing DCEP to the market, the expert believes.

In addition to domestic use, China may use the digital yuan to squeeze out the US dollar, which dominates international transactions.

For this DCEP must, in particular, become a competitor to SWIFT.

In addition, as former IMF chief economist Kenneth Rogoff argued, one of the directions of the digital yuan's expansion abroad is the underground market.

The 2022 Winter Olympics could be a likely field for DCEP testing in foreign audiences.

As for the largest economy, the United States,

The Block says the Fed is still taking a "conservative approach" towards CBDCs.

|

n e w s @ TradingCBDC com

no spaces. |